The benefits of life insurance for small to medium sized businesses.

The benefits of life insurance for small to medium sized businesses.

Learn what you need to know about Five+ Group Income and Life Insurance. Explore the features, benefits, and how it can assist the financial well-being for small to medium sized businesses (SMEs) along with their employees.

No small business wants to lose staff unexpectedly for health reasons, but in reality, it can happen and, in some cases, for an extended period of time – which can be detrimental to a SME business. It’s a risk that has had limited solution options – until now.

For quite some time, Financial Advisers have had difficulty obtaining Life and Income (protection) Insurance for SMEs because historically, the more traditional life insurers have not offered group insurance to this part of the market.

At Integrity, we look for ways to best support Advisers and their clients – because they deserve the best. We believe there is a better way to do life insurance and we are committed to doing just that.

Integrity have developed a group insurance product specifically for the SME market – Five+ Group Income and Life Insurance. A product like no other. A product that’s been co-created with Advisers like you for what the market needs. A product that’s efficient, sustainable, and cost-effective.

Our Five+ Group Income and Life Insurance product (unique to the Australian life insurance market) combines Income and Life Insurance in the one product. it was designed specifically for SMEs with 5 to 50 employees. It’s the first group product (of its type) to offer an income benefit to the employer, as well as the employee, and includes Death and Terminal Illness cover within the same contract. Plus, it can be purchased and maintained online.

Traditionally life insurance has not been available to support SMEs of less than 20 employees because of the traditional product structures offered by insurers – but with a simple product design, unique administrative process and streamlined technology platform, we at Integrity have met this challenge. Our solution supports businesses with life insurance protection for the impact of losing key staff to sickness, accident and / or injury along with protecting their most valuable asset, their employees.

“Everybody gets sick some time and to have that taken care of by the employer

I think that is nice” – Research participant

The advantage of Five+ Group Income and Life Insurance.

- It’s the first of its kind in the Australian life insurance market.

- Available for as few as 5 and up to 50 employees, supporting businesses that want to protect their employees, with all employees (including casuals) being covered under the policy

- It’s an ‘off the shelf’ product that combines Income and Life Insurance.

- There’s no minimum premium.

- Ability for Advisers and Brokers to instantly quote, with a straight through application process.

- It’s new event cover with no health questions being asked when purchasing the product – which means no individual Underwriting.

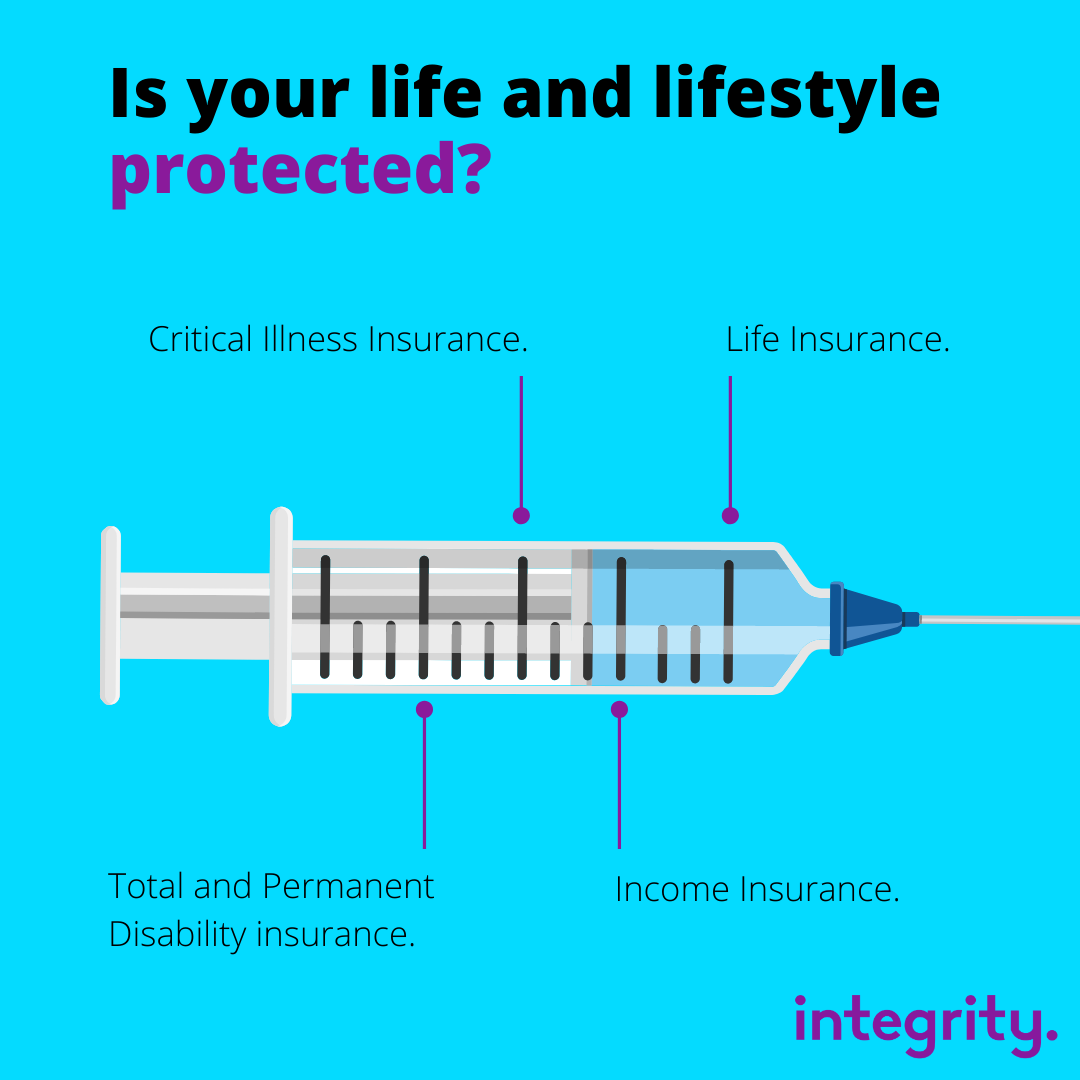

- A unique Death and Terminal Illness benefit of $200,000. Plus, an Income benefit of up to $10,000 per month, with 80% paid to the employee and 20% paid to the employer to assist with any additional costs to their business. With a Benefit Period of 1 year.

- A compelling price point, usually between 1% and 2% of salary.

- Advisers can choose to receive a level commission of up to 27.5% including GST.

- For more information, check out the Five+ Group Income and Life Insurance PDS.

“The main thing for me is that it is a differentiation tool as a business owner…How are we different from other firms, very tangible way to show how we view ourselves in relation to employees” – Research participant

Integrity Life

From the newsroom

Why insurance is important for small businesses.

- Attract and retain top talent – insurance benefits within an employee benefits package can provide employees with security.

- Mitigate the struggle to pay an additional salary – paying two salaries (the sick employee and their replacement) can be costly, especially as sick leave gets used quickly and worker’s compensation doesn’t cover sick leave or injuries that occur outside of work. This insurance product will benefit both the employee and the employer during these circumstances.

- Support employees – this product pays sick and / or injured employees for an extended period of time (80% of their salary taxed at their marginal tax rate and 20% is provided to the SME business), with rehabilitation and retraining activities helping them to return to work sooner.

Who is best placed to benefit from Five+?

When speaking with Adviser, we found that the ideal target market for a combined Income and Life insurance product is:

- Independently owned/founder run SMEs, with a mature business that’s operated for three or more years.

- They have 5 to50 employees, the majority of which are full time staff. The business is within a competitive market for good talent and as a result value employee benefits that’ll differentiate them in market.

- Their payroll process is automated.

So, what should you do next?

Get in touch with one of our BDMs at sales@integritylife.com.au to understand how Five+ can support the growth of your portfolio.

The product is a unique way to provide even better support to your SME clients – even those with just 5 employees. And if your client exceeds the maximum employee number for our group Life and Income (Protection) Insurance cover or have additional needs, our team can support with our Group Corporate Insurance option.

About Integrity Life

So far, we’ve been trusted to protect over 190,000 Australians from all walks of life. We’re committed to being your Partner today, tomorrow and for life. So, what are you waiting for? Go all out and get in contact with the team at Integrity Life at sales@integritylife.com.au for a fresh alternative to the more traditional providers.

This information has been prepared without considering your or your client’s personal objectives, financial situation or needs. Before acting on it, please consider its appropriateness to your circumstances. Refer to the relevant Product Disclosure Statement for full benefit details, terms, conditions and exclusions.

")